A couple of months back, I enrolled myself in a Fintech Course offered by MIT and GetSmarter . I definitely recommend this for anyone who is a avid enthusiast of FinTech and is really passionate about being part of this emerging field. Although, in the past few years, I’ve interacted with several of the products and technologies that have started in the area, mainly in the payment, personal finance and remittances space, I’ve never really explored beyond being just a consumer and an avid enthusiast. As it turns out, there was a lot more to FinTech than just money and payments.

I was particularly intrigued by the digital identity space and the advances that have taken place in the field. Albeit being slow in adoption, through my course I realized that it is a field that has seen the emergence of several startups and perhaps gotten a lot more interest over the past few years.

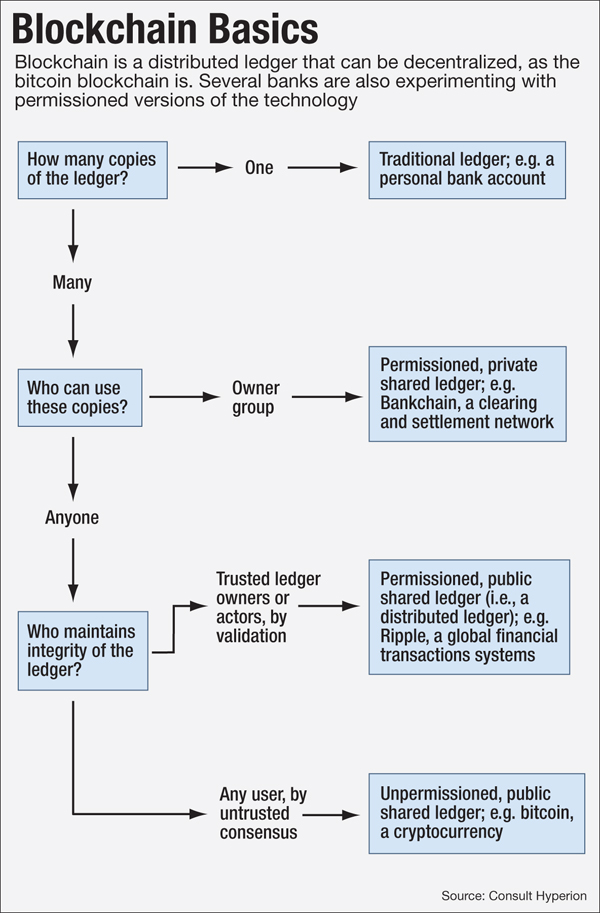

A quick search on the google search stats shows that the trend on digital identity have been on the rise since the turn of this year. There are several aspects attributed to this. Emergence of bitcoin is seen as one of the primary drivers. Bitcoin uses an underlying technology what is called as Blockchain. Blockchain in a layman’s terms is a transaction log technology that was originally built as a public ledger for all bitcoin transactions, maintained as blocks. Its decentralized and unalterable nature made it an immensely popular technology among financial geeks. Soon it grew from the public permissionless bitcoin blockchain to private and permissioned blockchains built for enterprise. In a nutshell, this figure describes blockchain.

Digital identity like many other themes in FinTech has found quite an interesting partnership with blockchain. There are some aspects of blockchain that can prove to be extremely useful in digital identity. A primary roadblock for the widespread adoption of digital identity is trust. Consumers and businesses have to trust the privacy and security of any digital identity solution. Know Your Customer (KYC) as banks call it, identity is verified by every bank every time there is a new transaction between a bank and a customer. The overhead associated with it in a digital era can possibly be be solved by a private blockchain based identity system .

Now imagine a digital world where a consortium of such private blockchains can prove the identity of a person. Imagine also a world where you now don’t have to use a paper form of identity to start an account, move across borders or even simply enter a bar. There are several challenges to making this a reality. My previous post on the regulatory challenges is just one of them. As I finagle through this world of digital identity, I plan to keep posting more.