Digital identity is seen as an integral enabler of the Internet of value. Over the past 5 years, digital methods have increasingly become the preferred means of transactions, that include payments, remittances etc. Statistics point out that in a traditionally cash friendly country such as India, digital transactions have exceeded the cash transactions in FY2015. Studies have analyzed positive impact of digital identity on GDP, tax and employment. A recent study by Boston Consulting Group points out that digital identity can bring governments across the globe up to $50billion in saving by 2020. This growing prevalence of digital identity brings along the need for regulatory measures to ensure that the information is handled responsibly by both private and public sectors.

While trust is a primary factor for digital identity to succeed, there exists a need to validate or ensure an identity claimed by individuals involved in a transaction. Several regulatory bodies have been initiated by countries across the globe to regulate this validation. In United States, National Strategy for Trusted Identities in Cyberspace (NSTIC) has taken up the initiative to create secure online identities for Americans. EU formed the eIDAS for the development of regulations on digital identity and UK started the Identity Assurance Program (IDAP) which is a government certification program to authorize private sector companies to act as digital identity providers.

Regulations and the initiatives started so far in this space are good for the adoption of digital identity. They cater to the two important reasons for the need to regulate, viz uncertainty and public good3. Public need to be assured that their identity is safe with the identity holder. They also need to be confident that, in their transaction with their peers, they have a valid and trustworthy digital identity to validate. Hence in my view, the regulatory initiatives so far address the primary concerns of the public.

However, the problem also arises when there is a need for cross border transactions. Paper identity has clear boundaries; like a driver’s license in your country being exclusive to your country. They are also regulated well by the government with valid background check. Digital identity on the other hand has loose boundaries in the Internet world. Also, different countries have different visions on what an identity is and how they can be regulated, albeit it all ultimately gets accessed globally. The challenge for the growth of a venture in Digital Identity will be due to the fact that there is no common consortium that can regulate identity globally.

Challenge also lies in the fact that banks continue to be the party responsible for the identity, albeit it being issued by the states and countries. Although there have been measures to create a private sector worldwide identity and authentication system (FIDO – Fast ID Online), the adoption has been slow.

Digital Identity is the key to the growth of digital economy and Internet of Value. A comprehensive regulation carefully crafted to avoid too-big-to-fail ventures, such as the passport systems regulated by ICAO (International Civil Aviation Organization) ICAO (International Civil Aviation Organization) can go a long way in enabling a paperless digital world in the future.

Tag: “Digital wallet”

What’s in your wallet?

Ever since its inception back in the 1920s, with oil companies and hotel chains, credit cards have been a victim of constant identity thefts. Easy as the payments were, equally easy was to lose it, stolen or left behind in a bar/restaurant. I had written sometime back about Digital Identity . While the idea then was about a digital wallet on your smartphones using NFC or Near Field Communications, Coin decided to take it a step further. NFC still in its infant stages, mainly due to the security concerns associated with it, Coin might just be an answer to a fat wallet! In short, coin makes a digital copy of all your credit cards and lets you swipe “the coin” in place of them. And what’s more, it constantly communicates with your smartphone via bluetooth. This ensures that you always have the coin right next to the phone for it to function, with an alert triggered every time it leaves the phone behind by around 7 meters. It then deactivates itself – a simple solution for a lost of stolen card. Sounds wonderful on paper.

Two reasons why adopting such a technology would make me a little skeptical, although I must admit I’m usually always the first to pounce on any new gadget. For one, this is a financial gadget literally having access to every single credit card that you choose to store in there, much like a financial management tool, which gets to have all your financial data. And, although it was announced back in November, this year. The shipments will not start until “summer” of 2014 and you are charged as soon as you preorder. Now the company has a very diplomatic answer to this, stating that this is a way they can help aid, financially, the manufacturing process. I’m sure this is all very credible, with its all expanding media hype and the number of preorders.

Julianne Pepitone, from CNN Money, puts it very nicely on 3 big problems with Coin . I would say, one of the primary problems (in fact two in her article), makes me nervous – its acceptance amongst the retailers and credit card companies. Consumers will accept this readily as long as the usability is widened. It would be harsh if you enter a shop and the retailer does not accept your “coin”. Common man does not usually take security as a huge threat unless there is a gaping hole. If not several of those startups such as mint.com, paypal, or even facebook, wouldn’t have taken off.

Having said all those, I still think Coin has a lot of potential. For one, the concept in itself is interesting. Not having to carry all my credit cards in my wallet just reduced the significance of my traditional wallet entirely. And the card looks great in its design.

So while we wait on its shipments and the user reviews, I’m still on the fence regarding the preorder… Let me leave you with an interesting concept video in the meantime.

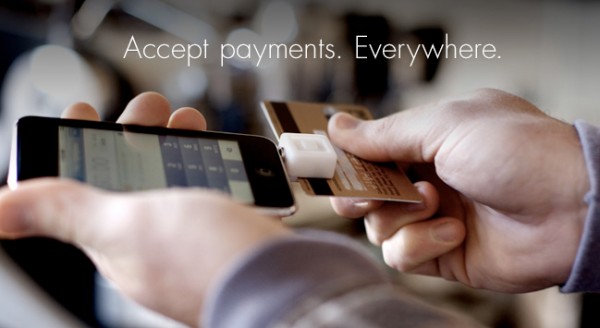

Digitizing the cash counters

I’m sure the image that you see above has become quite a familiar sight across America. Apple stores have been flaunting a similar version for quite a while now, which almost resembles the Mophie . I first noticed this at Conshohocken Cafe , a quaint little breakfast place at Conshohocken, PA. Square , as they call it, they started to make money through the 2.75% transaction fee charged per swipe. Now my post was not particularly to about the Square, but instead, the Square Stand , that was announced today. At $299 a piece and a $499 iPad, this can replace the traditional cash registers in a blink of an eye. Sounds quite simple, as we start to see more and more dependency on the mobile device .

But wait, there is more. The exact same day, Paypal decides to announce its revolutionary product know as the Cash for Register . With a free credit/debit/paypal processing for the rest of the year for any qualifying US Business, we now have a competition!

The era of cash registers which opens up a “slot machine” of quarters and pennies is slowly disappearing. Whether its paypal or square, the digital revolution has spared none. Soon the traditional cash registers will just be a piece of antique in the museum!

Amazon Coins – The era of virtual coins begins here (?)

Imagine a world where you trade your dollars for virtual money. You keep a track of the conversion rates as you move from one site to the other. Imagine what it would be like when credit cards show you credit limits in terms of virtual money. And what if your credit card itself is virtual?

Back in 2005, Philip Rosedale, the founder and CEO of Second Life, gave an interesting interview . He said “The GNP of Second Life in September 2005 was L$906,361,808 or U.S.$3,596,674, based on the recent L/U.S. exchange rate”. Now the interesting idea there is L/US Exchange rate. The rates varied just like the conversion rates for real money.

For this same reason, when Amazon announced their “Amazon coins”, I was excited. Now obviously, with spending amazon coins also comes earning amazon coins, a free ride for app developers on Kindle. And of course the whole saga of tax revolt could soon follow.

Now if you take a step further, lets say iTunes starts to go down that path, with Apple coins and so does ebay. And if the rest of the “world” follows suit, you now have a “real” virtual world, with “developed” sites, “developing” sites and “under developed” sites. You could have virtual banks, which loan Amazon coins at a 0.9% APR and of course as you transact between sites, you could watch a daily ticker of conversion rates.

I guess I’m overthinking here. Maybe it’s an overdose of caffeine taking its effect. But Amazon coins do seem like a promising step towards a virtual economy.

Wallaby solves one of those financial dilemmas!

If you are someone like me, I’m sure you must have faced a situation where you took out your wallet at a restaurant and started to gaze at all your credit cards wondering which one to choose in order to gain the maximum rewards. Well, now the answer to this problem is just a click away – Wallaby ! Currently launched just on the iPhone as a free app, wallaby lets you add you credit cards to scrape through their rewards and benefits every time you search for a location. Before you panic, I must say, it does not require you to give out your entire card number. All it needs it the first 6 digits of your card, which uniquely identifies the bank and their list of credit cards. You can then save the ones you own. What that means is, wallaby just mines the rewards programs from each of those cards, which usually stays the same across any user. So the next time you go to a restaurant, all you have to do is to just launch the app and it will tell you based on your location, which one of those cards to pick to pay. Quite a novel idea!

Coached by the mentors at Mucker Lab , the app was launched two days ago at the iTunes Store . While the whole array of credit cards that it presents to you is huge, there is still quite a few missing. For now, it gives you an option to send a message stating the details of the missing card. I’m sure as the user base grows, the database of credit cards will slowly move towards being exhaustive.

The era of digital identity

MacRumors announced yesterday that Apple won the patent for Near Field Communications based iTransport , an app that could transform the way the world identifies you! Although this was long pending, there was an air of unusual caution thrown by Apple in regards to the concept of mobile payment. So when Passbook digital wallet app was announced as part of the iOS6 last month, I bet there was a sigh of relief among the Apple fans, who were on the verge of losing hope. According to MacRumors, there was also an unexpected level of details put forth by Apply as part of the patent for an application that still remains a concept, perhaps due to the sensitivity of the materials that it may potentially contain in the future – credit cards, passport data, driver’s license, what all and what not.

The concept of digital wallet is not new. It’s potential was identified back in 2004 when Nokia, Philips and Sony established the NFC Forum . And in 2010, Google along with Samsung announced the first NFC enabled phone – a Samsung Nexus S running on Gingerbread version of Android . Near Field Communication, or NFC as it is lovingly called, is a protocol used in smartphones, or any mobile device for that matter, to establish a two-way communication between each other, when touched or brought within a close proximity. Unlike the pairing in bluetooth and the configurations in a Wifi communication, NFC’s ease to setup is perhaps its best selling point. In 2005, Mastercard started rolling out EMV (Europay Mastercard Visa) compatible wireless payment feature through its MasterCard Paypass and it spread like wildfire with banks latching on to the paypass feature on their credit cards. But it was not until 2011 when google announced its Google Wallet , that the concept of using mobile phones to make a payment “without a swipe” started to take shape.

Soon it burgeoned, through key fabs, mobile tags, and of course the smartphone apps. And with iTransport, this “magical” concept might just be elevated to whole new level, if digital documents become a reality. Now, before you go dreaming any further, there are quite a few obvious challenges, one of them and perhaps the biggest of them all being the security threats that it can impose. Being able to wirelessly transfer a passport, a driver’s license or a social security information can present a happy hunting ground for identity thieves . And that in itself can make its acceptance among common man (consumers as they call it) a herculean task. So going back to what I said earlier, Apple coming forward with a rather unusually detailed patent on its iTransport application could just be a way to build that confidence amongst the consumers. Or would it just open up a whole new can of identity theft crisis? I guess only Time can tell what is in store…